STEP 1: Understand Original Medicare

A Zolezzi Insurance agent will answer your Medicare questions.

Step 2: explore your medicare options

There are several Medicare plans available in Oregon for you from.

step 3: choose your plan and enroll

We can help you choose the right plan and enroll when you are ready.

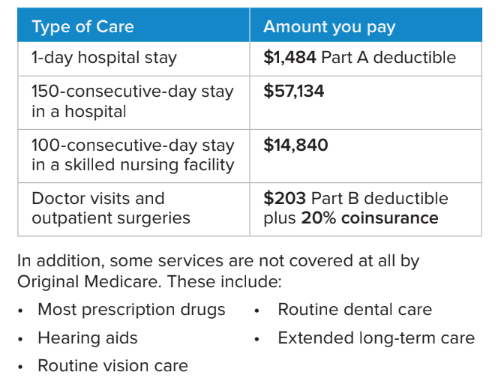

What does this mean to you?

Original Medicare is a beneficial program that helps ensure that the health care you need is covered. But you still could be left with thousands of dollars of out-of-pocket medical costs. Examples of your costs with Original Medicare:

Now that you’ve reviewed your Medicare benefits and options, you’re ready to dive in. Learn about the best times to enroll so you can avoid penalties and get the type of plan you want.

Your Initial Enrollment Period is a seven-month window—from three months before your birthday month to three months after your birthday month.